The $300 million HPC deal for Cipher Mining (CIFR) was alleged to be a catalyst, however stock lay down because the $1.3 billion convertible elevate stole the highlight. Right here's why the establishment hastened and what it means to shareholders:

The subsequent visitor put up comes from bitcoinminingstock.io, A public market intelligence platform that gives knowledge on firms uncovered to Bitcoin mining and cryptocurrency methods. Initially printed by Cindiffen on October 1, 2025.

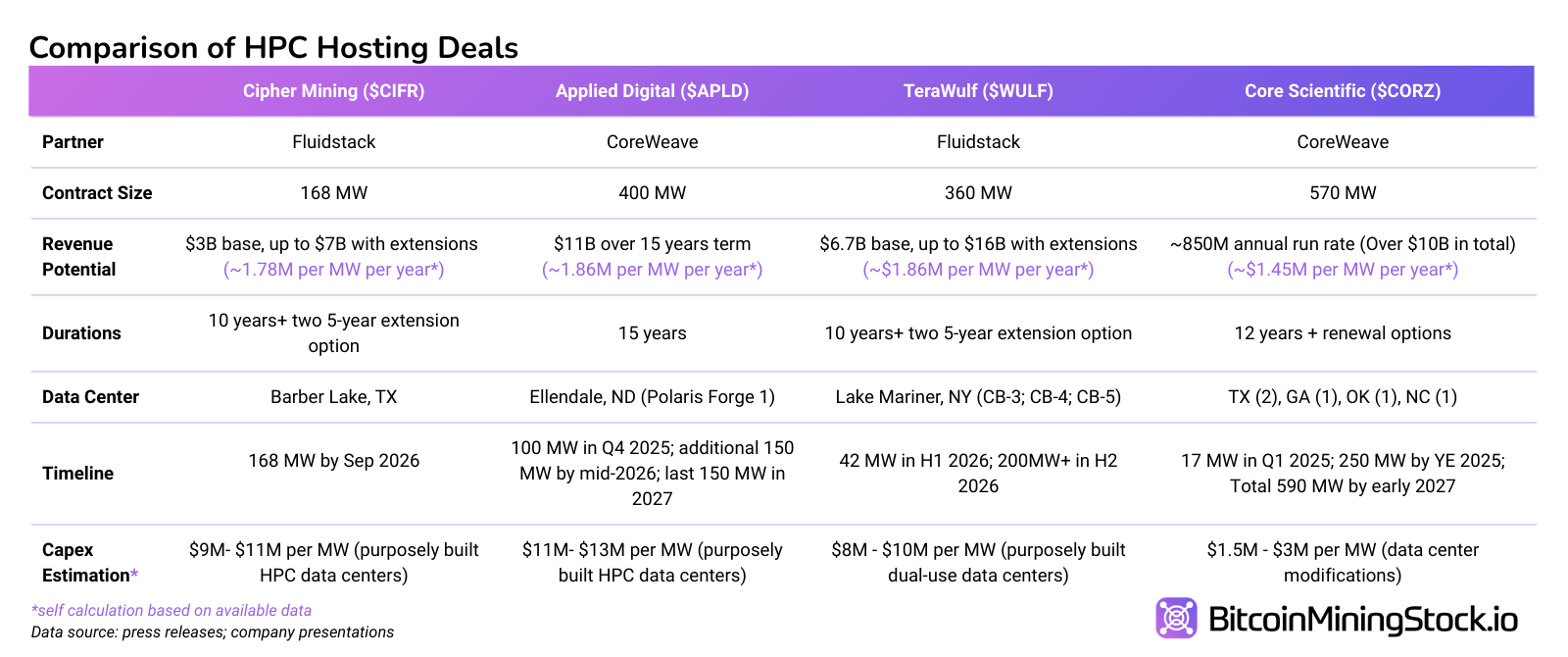

Latest Crypto Mining announcement The primary hyperscale buying and selling revealed Fluidstack as an HPC shopper. This marks the fourth main HPC internet hosting settlement amongst public miners and enhances the sector's pivot to HPC as a complement to Bitcoin mining.

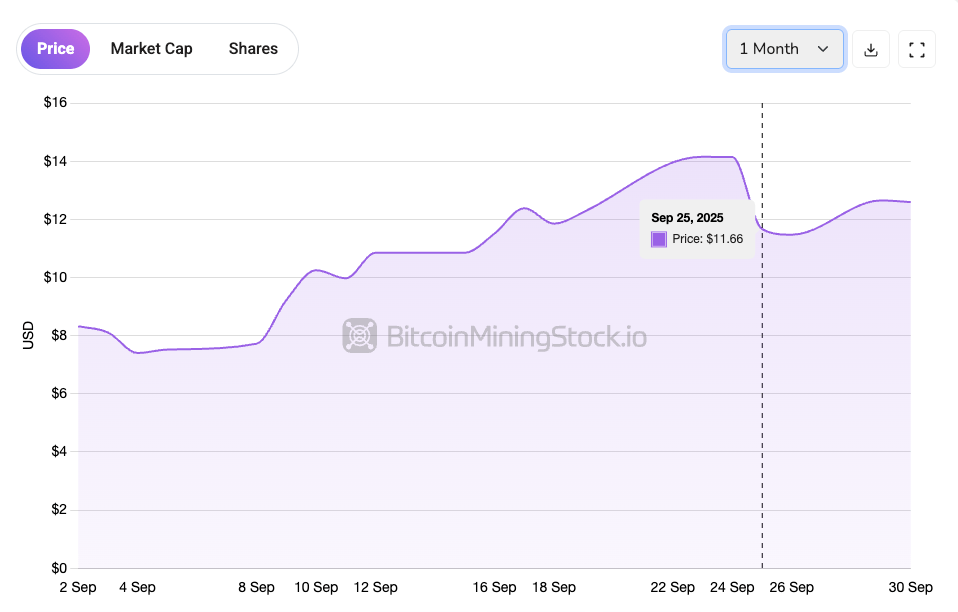

Such bulletins often trigger sustained gatherings. This time, Cipher's inventory was first checked, however rapidly fell after saying an enormous non-public finance. Inside 24 hours, $800 Million Non-public Convertible Observe Provide Up measurement $1.1 billion On overwhelming institutional demand. On social media, traders have denounced the convertible for killing momentum. This notion is comprehensible, but it surely additionally reminds us that enormous upfront prices are required to make the advantages of HPC/AI a actuality.

Let's unlock this mechanism of funding contracts. As a result of the establishment unexpectedly finds why shareholders responded cautiously.

HPC Economics and Funding Hyperlinks

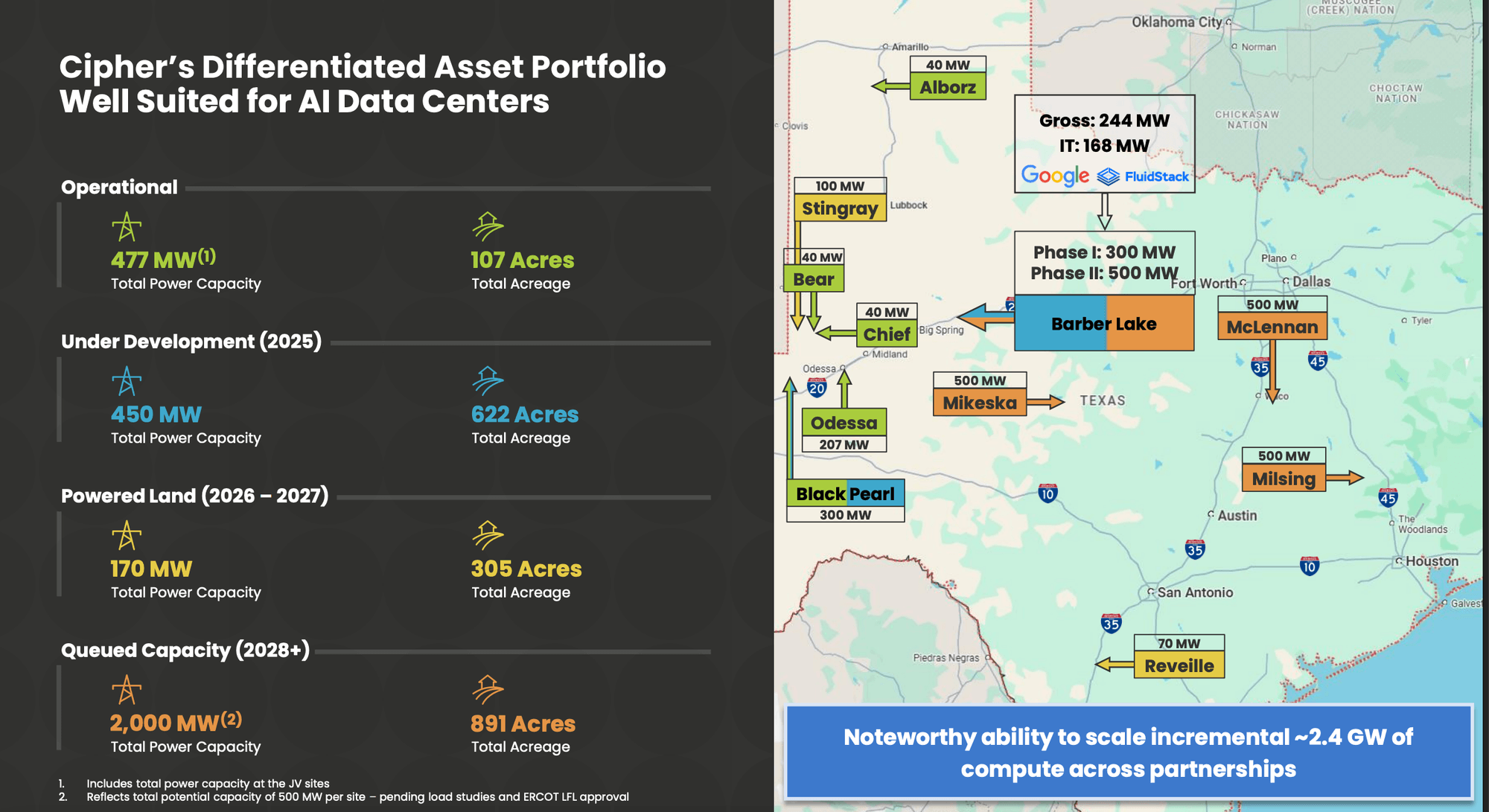

The Barber Lake web site and Cipher's wider 2.4 GW pipeline are the spine of HPC methods. You want Hyperscalers Giant pay as you go spending Land, energy interconnections, and knowledge middle build-outs. Fluidstack examined demand, however capital was a bottleneck.

*Barber Lake's 168MW construct alone is anticipated to require a capital funding of round $1.5 billion to $1.8 billion, even earlier than making an allowance for the extra prices required to completely make the most of Cipher's wider vitality pipeline.

That's the place the convertible is available in. A $1.1 billion wage enhance isn’t an afterthought to HPC tales, however a obligatory step. By securing years of capital with zero curiosity, Cipher bought the time and assets to run. However in doing so, administration shifted danger from administration to fairness construction.

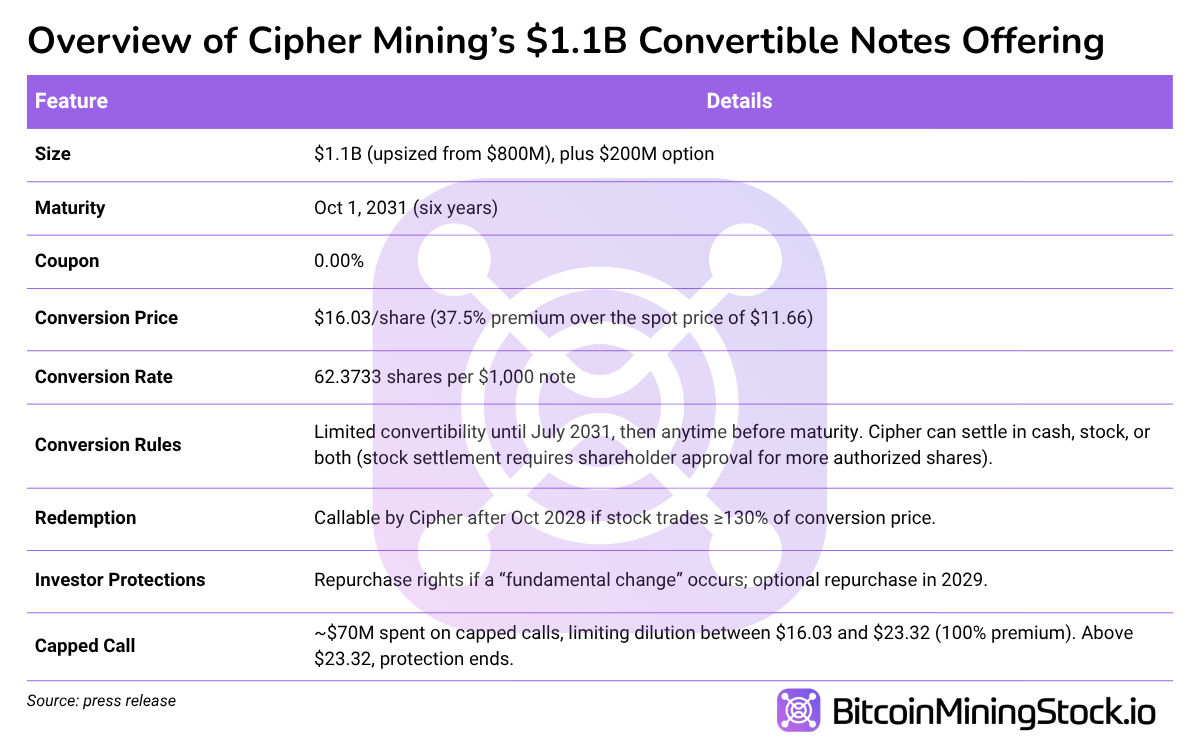

Disassemble the convertible observe

Worth of value 0.00% Convertible Senior Notes Till October 1, 2031It’s scheduled to be resolved on September thirtieth, 2025. The deal rapidly rose from $800 million to $1.11.1, with an extra $200 million possibility*, reflecting overwhelming institutional demand.

*$200 million buy choices exercised per cipher Type 8-Okconvey within the complete convertor payments issued to $1.3 billion.

In comparison with peer miners, the transaction (6-year funds at 0% rate of interest) seems to be cheaper. Some individuals both paid an rate of interest of 10% or extra on their debt or depend on issuing cereal fairness. As well as, Cipher spent $700,000,000, Cap name transactionwhich helps cut back dilution when inventory rises. In different phrases, shareholders are shielded from dilutions of as much as $23.32 per share (nearly twice the promoting value reported on September 25, 2025).

Why did the establishment run in?

At first look, this non-public product doesn't pay curiosity till 2031 and doesn't appear engaging to be locked. Nonetheless, convertible notes are usually not easy bonds, however primarily Mortgage and Inventory Name Choices. Traders will obtain compensation in 2031 if crypto is struggling, but when the inventory exceeds $16.03, they will convert pretty and seize it the other way up.

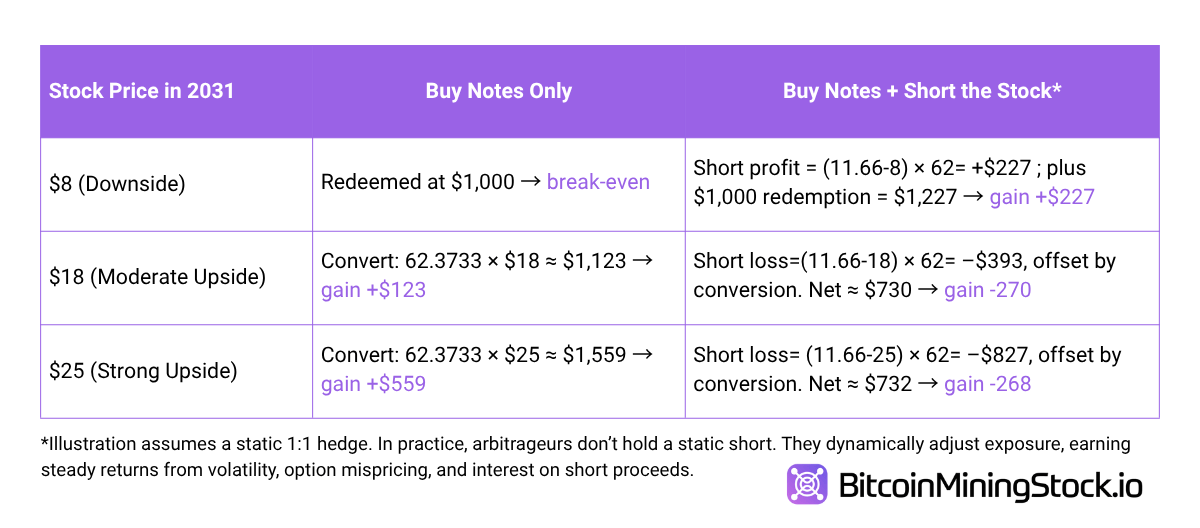

For hedge funds, enchantment goes past easy long-term publicity. Many runs Transformable arbitrage methodsthey purchase notebooks and shorten the inventory proportionally to conversion price. After that, the brief hedge is like that It's dynamically adjusted As inventory costs transfer. The purpose is to not guess on the fundamentals of an organization, however to make income from options-like buildings and inventory volatility.

To clarify, we assume that the investor will purchase $1,000 face worth Notes (62.3733 shares if transformed). Cipher's inventory was $11.66. The conversion is $16.03.

in Static setupthe result’s as follows:

So, what does this imply? Static arithmetic could seem unattractive to arbitrators at increased costs, however dynamic hedging makes the technique worthwhile throughout the end result. That's why the establishments stack up: they get the construction they supply Safety like the other way up bond like choices,Then again, extraordinary shareholders solely profit if Cipher is efficiently executed. This explains why this transaction took impact inside hours.

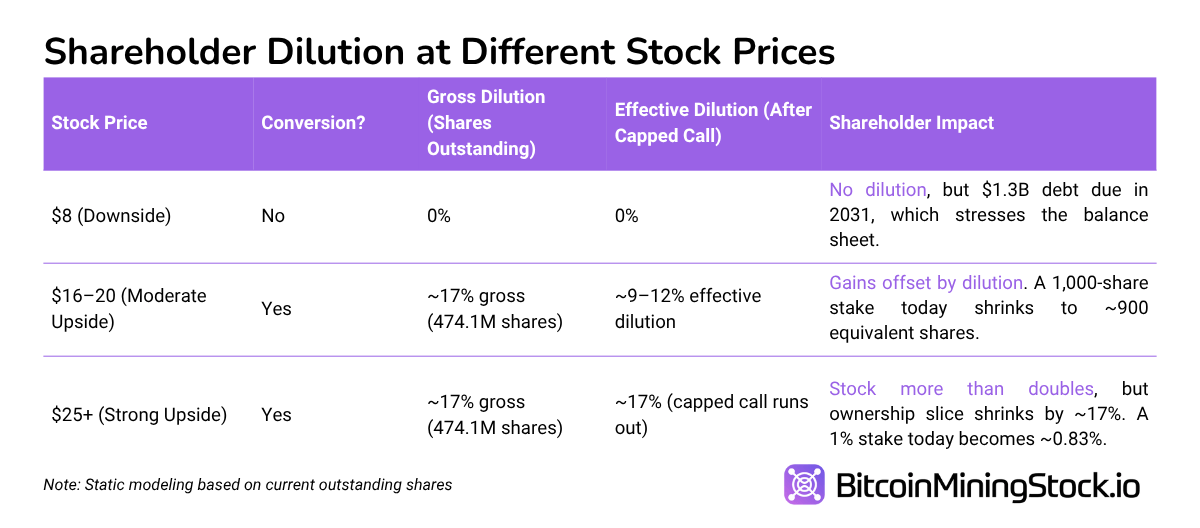

Dilution mechanism for shareholders

For a typical stockholder, the impression is easy and it’s a lot much less versatile than an establishment. Cipher presently has ~393m shares are unpaid. If all notes are transformed, a brand new inventory of ~81.1m will likely be issued and the whole will likely be lifted to ~474.1m. Capped calls trim this 9-12% If the shares land between $16.03 and $23.32, however exceed that (>$23.32), there is no such thing as a safety and the shareholders will take up the complete dilution.

Asymmetry Right here: Establishments can fine-tune dangers by means of hedging and lock in to return, however shareholders can’t. Inventory traders have binary outcomes. The code is working and the inventory has been valued effectively sufficient to exceed a 9-17% dilution, or not, with the corporate being responsible for shares and $1.3 billion in debt.

Closing Ideas

Cipher's Fluidstack contract I'll confirm it A strategic shift in the direction of HPC and AI internet hosting. Like Core Scientific, Utilized Digital, and Terawulf, the corporate is leveraging vitality and infrastructure to draw hyperscale shoppers, aiming for a way more predictable income stream than pure Bitcoin mining.

However muted inventory reactions present how Funding Even probably the most optimistic headlines might be forged a shadow. The $1.3 billion convertible observe has well structured, capped name safety with out rapid money drainage, and nonetheless represents a considerable future declare for equity. Shareholders face a dilution of 9-17% when the cipher is executed, however that's true Dilution solely causes a considerably increased inventory value.

This stress explains the divergence HPC buying and selling is a transparent strategic victorynevertheless, fundraising restructuring traders deal with danger. Cipher is the front-load capital to construct Barber Lake and activate the two.4 GW pipeline. This can be a obligatory step if you wish to monetize HPC demand at a big scale. If the execution takes place throughout the deadline and Barber Lake's 168 MW comes on-line by September 2026 as deliberate, the ensuing income might exceed the dilution.

For now, convertibles give establishments an entry level like low-risk choices, with shareholders taking execution danger. The HPC storyline stays participating, however till concrete revenues come true, the market can have fewer cryptos attributable to its Fluidstack offers, and the $1.3 billion funding it has been used to fund it.