The UK’s bond unrest as soon as once more calls into query the very function for which Bitcoin was created: sovereign debt and belief in monetary administration begins to crack.

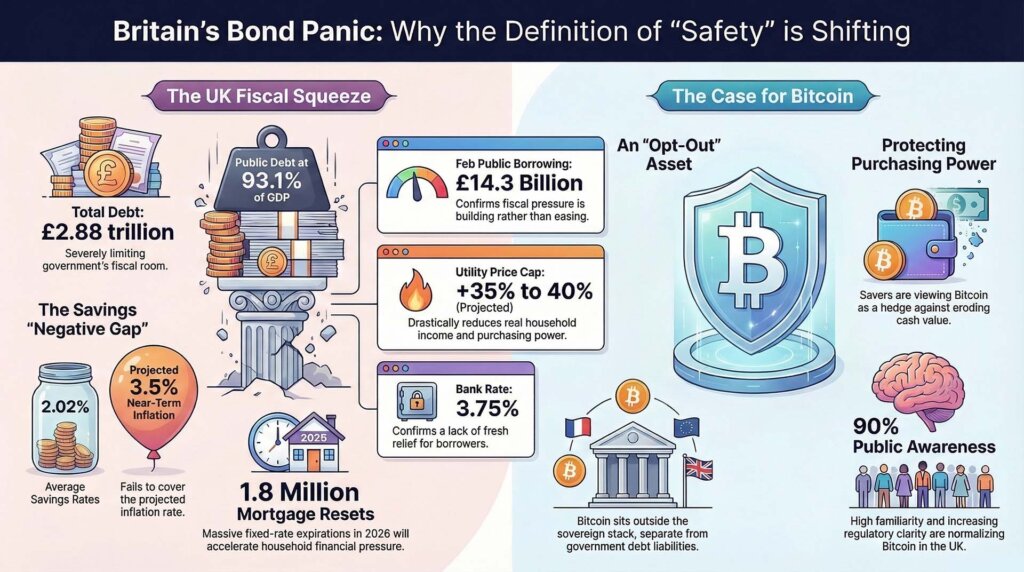

Britain's fiscal pressure deepened after official borrowing knowledge confirmed public sector web borrowing rose by £2.2bn year-on-year to £14.3bn in February, making it the second-highest February determine since information started in 1993.

Web public sector debt reached £2.88 trillion, or 93.1% of GDP. On the identical day, the Financial institution of England stored its financial institution charge unchanged at 3.75%, warning that the current power shock would trigger inflation to rise once more over the approaching quarters, similtaneously gas and utility payments for households would rise.

The rapid market response is on authorities bonds, rate of interest expectations, and mortgages. Gradual modifications seem in financial savings conduct. The UK doesn’t must rush into Bitcoin for belongings to enter the dialog in new methods. New doubts about money, authorities bonds and the sluggish tempo of charge cuts are sufficient to alter the best way savers rank dangers.

That change begins with arithmetic, not ideology. The Financial institution of England stated in its newest minutes that preliminary employees forecasts are for CPI inflation to be between 3% and three.5% within the coming quarters. He additionally expressed the view that will increase in family gas and utility prices will put stress on actual incomes. By January, the typical rate of interest on family prompt entry deposits was 2.02%, in accordance with the central financial institution's personal knowledge.

The simply accessible money funds are due to this fact decrease than the central financial institution's personal present expectations for inflation. The distinction is evident, roughly 0.98 to 1.48 proportion factors under the short-term CPI path. For savers, the definition of security begins to alter from there. Money nonetheless protects nominal worth. It does little to guard buying energy.

The UK house channel can be making fast progress. The UK Treasury's newest forecasts estimate that round 1.8 million fastened charge mortgages will finish in 2026. The Workplace for Nationwide Statistics has already proven in its Family Value Index that inflation will probably be 3.6% for all households and three.7% for mortgage holders within the fourth quarter of 2025. This was introduced earlier than the central financial institution just lately warned that power costs would push prices up once more.

The chain of occasions within the UK runs by means of authorities borrowing, the re-pricing of gold and silver, and family funds. Gilt doesn't appear very calm. Simply accessible money undercuts short-term inflation paths. Mortgage ache will hit much more households as fastened contracts expire.

Bitcoin is gaining relevance in that setup as savers think about whether or not smaller belongings exterior of the sovereign stack must be included within the combine.

| indicator | newest figures | How the saver conduct modifications |

|---|---|---|

| February public borrowing | £14.3 billion | Exhibits that fiscal pressures are nonetheless growing somewhat than easing |

| public debt | 93.1% of GDP | There’s restricted room for a clear fiscal reset. |

| financial institution charge | 3.75% | Confirms that banks didn’t present new aid |

| Central financial institution’s short-term CPI outlook | 3%~3.5% | Factors out new pressures on actual incomes |

| Deposit charges for fast entry | 2.02% | Simple money stays under banks' inflation vary |

| Mortgages will probably be reset in 2026 | 1.8 million | The affect of rising rates of interest on family funds will speed up |

The squeeze begins with money stream and extends to portfolio selections.

The Financial institution of England's newest rationalization of the shock offers cross-market context. In a March assertion, the Financial institution highlighted that round a fifth of worldwide oil and LNG provides sometimes move by means of the Strait of Hormuz, that Brent crude and Dutch TTF gasoline costs have been round 60% above pre-shock ranges, and that UK gasoline futures steered the following Ofgem cap might rise by 35% to 40%.

That is the bridge between macro knowledge and retail savers. Until households change the best way they consider cash, the federal government might run large deficits for years. Nonetheless, your utility invoice will skyrocket each month. Mortgage resets will be accomplished by letter and direct debit. That is the second when savers begin weighing the trade-offs between buying energy, liquidity, volatility, and belief within the issuer.

This distinction is beneficial as a result of whereas Bitcoin fell by roughly 50% from October 2025 to February 2026, choices volatility rose to its highest degree since 2022. Even throughout an lively squeeze, buyers are nonetheless promoting risky belongings to lift money. Bitcoin stays delicate to liquidity stress throughout these intervals.

This sample additionally reinforces the long-term nature of Bitcoin on this UK transfer. Authorities bond costs are risky, expectations for rate of interest cuts appear additional distant, and yields on simply accessible money are decrease than the central financial institution's present expectations for inflation. Underneath these circumstances, Bitcoin begins to look extra like an opt-out from the promise of a nationwide forex than pure hypothesis. It has its personal volatility and totally different sources of danger than these presently dealing with money and Treasury bond holders.

The UK regulatory regime makes that dialogue simpler than it was just a few years in the past. Consciousness of cryptocurrencies is over 90%, with 25% of crypto customers saying they might be extra prone to put money into them if the market have been extra regulated, in accordance with the Monetary Conduct Authority's newest shopper survey.

The findings assist asset class information and sensitivity to regulatory readability. This leaves the dimensions and timing of recent demand unresolved.

The UK can be noteworthy exterior the UK as a result of the family mechanism is unusually seen. The US nonetheless dominates crypto flows, ETF headlines, and greenback liquidity. Nonetheless, the UK reveals stress factors sooner.

When debt mounts, borrowing takes an surprising flip for the more serious, utility payments go up, and huge mortgages are headed for reset, this drawback will attain your plate sooner. What cryptocurrencies signify is a widespread willingness to deal with sovereign banknotes and financial institution deposits as an imperfect reply to the phrase “protected.”

Official forecasts are additionally pointing in the identical course. In its March outlook, earlier than the shock, the OBR had anticipated 10-year authorities bond yields to be 4.5% and 30-year yields to be 5.3%, whereas web public sector debt was anticipated to rise from 94.5% of GDP in 2025-26 to 96.5% in 2028-29.

The tax burden is anticipated to rise to 38% of GDP by 2030-31. These numbers present continued fiscal stress, leaving little room for a comforting model of the outdated technique of slicing rates of interest, calming bonds, and affected person savers working collectively to resolve issues.

What does the following 12 months seem like?

Every believable path for subsequent yr has a unique affect on saving conduct.

The shock wears off, but it surely doesn't come again.

The central financial institution's 3% to three.5% inflation vary will show about proper within the coming quarters, with utility payments rising and households rebuilding their reserves, though actual income stay low.

In that model, Bitcoin will acquire a story foothold, however might not be capable to entice giant flows. The case is easy. When money is liquid however loses buying energy and bonds are not benign, non-sovereign belongings look simpler to justify as a part of a broader financial savings combine.

Power shock continues

The Nationwide Institute of Financial and Social Analysis has modeled a sustained shock state of affairs through which UK inflation rises by 0.7 proportion factors in 2026, GDP falls by 0.2 proportion factors in 2026 and 0.3 proportion factors in 2027, and financial institution rates of interest find yourself round 0.8 proportion factors above the benchmark.

Earlier than the most recent transfer, NIESR's winter forecast had the financial institution charge at 3.25% by the tip of 2026. Taken collectively, these ranges ought to keep a path above 4% even when the shock continues.

That’s the state of affairs most probably to deepen the Bitcoin case. Excessive debt reduces fiscal house. Money decreases as a result of rising inflation. Rising long-term rates of interest will hit house loans. This mixture will increase curiosity in belongings exterior of nationwide debt, though Bitcoin itself stays risky and delicate to broader market stress.

Stress in market functioning

The third path would harm Bitcoin within the brief time period and strengthen its attractiveness in the long run. A separate bond market observe from NIESR warns {that a} sovereign length shock might transfer from a repricing to a monetary stability occasion, requiring central banks to assist market functioning though inflation remains to be uncomfortable.

That’s the institutional contradiction that Bitcoin was designed to resolve. It's additionally the type of market interval that would nonetheless put stress on Bitcoin if buyers rush for liquidity.

This rigidity explains why the UK's current bond actions have been so putting. Enterprise is troublesome. The mechanism is evident. As nations borrow closely, power prices rise, inflation picks up once more, and households face mortgage resets, the social that means of safety begins to alter. The dialogue strikes from macro idea to month-to-month outflows and upkeep of buying energy.

The UK's current bond strikes might be a improvement for Bitcoin earlier than many People see it as such.

UK knowledge already reveals components of that: £14.3bn borrowed in February, debt to GDP at 93.1%, coverage charge held at 3.75%, short-term inflation getting back from 3% to three.5%, accessible money at 2.02%, 1.8m mortgages scheduled to reset in 2026.

None of those numbers counsel that Bitcoin will win anytime quickly. Collectively, these signify rising stress on outdated definitions of security.

If power costs stay excessive, the following utility invoice cap rises as futures counsel, and mortgage resets proceed to endure from excessive yields and sluggish rate of interest aid, extra savers might determine that money and authorities notes can not remedy the entire drawback.

(Tag Translation) Bitcoin