Final week, an institutional investor executed the most important single off-exchange commerce within the historical past of a U.S. Bitcoin spot-traded fund, draining a $1.26 billion place in BlackRock's iShares Bitcoin Belief (IBIT).

The deal has sparked intense debate on Wall Avenue, however NYDIG's evaluation suggests the sale was a focused emergency exit by the whale, relatively than the routine conclusion of a well-liked hedge fund arbitrage commerce.

Our evaluation exhibits that firms paid a excessive worth for immediate liquidity. Roughly $30 million in execution prices have been incurred simply to safe an exit earlier than the broader digital asset market fell right into a notable downturn.

Understanding IBIT MegaTrade

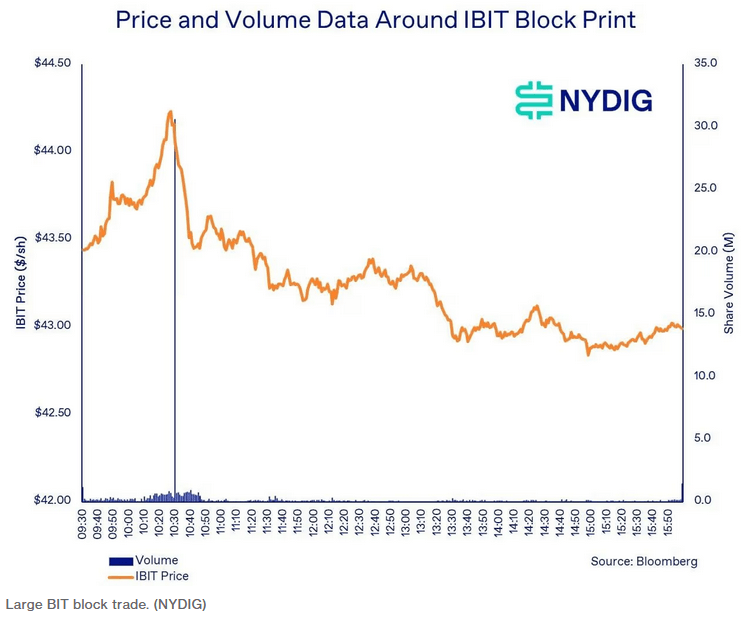

NYDIG famous that BlackRock's IBIT exercise started to quietly speed up after an early morning session at regular volumes.

In accordance with the corporate, the ETF's inventory worth slowly rose from $43.81 to an intraday excessive of $44.24 between 10:16 a.m. ET and 10:28 a.m. ET. Buying and selling volumes throughout this era soared to 3 to 4 occasions regular ranges, suggesting that executing brokers have been testing market liquidity and punctiliously getting ready for big orders.

Then, at precisely 10:30 a.m., the hammer fell.

A single vendor bought 29.21 million shares of IBIT inventory in a privately negotiated off-exchange transaction. The block cleared at $43.16 per share. The prevailing open market worth at that second was $44.17, so the vendor accepted a 2.3% haircut on the spot. In greenback phrases, that execution nice value the mysterious entity roughly $29.5 million.

The regulatory reporting code accompanying the transaction signifies that the vendor locations a particular emphasis on velocity. This commerce was output to the FINRA/Nasdaq TRF Cartelet. This cartelette is a facility utilized by broker-dealers to report darkish pool and privately negotiated transactions.

As well as, we additionally acquired an intermarket sweep order designation together with a Reg NMS trade-through exemption.

In layman's phrases, these exemptions permit institutional traders to keep away from the requirement to hunt the best possible listed worth throughout a number of public exchanges, topic to the accountability of assembly sure protected quotations.

This means that sellers actively selected the understanding of a right away, uniform exit over the potential of a greater worth.

Debunking the Arbitrage Fable

When extraordinarily uncommon multi-billion greenback prints happen in crypto ETFs, market commentators sometimes default to the frequent rationalization of foundation buying and selling.

This widespread hedge fund technique entails shopping for spot ETFs and shorting Bitcoin futures on the similar time, incomes yield from the value distinction between the 2.

Nonetheless, NYDIG's evaluation identifies three distinct elements that dismantle the premise unwind concept on this case.

First, the fundamental economics don’t agree. Foundation merchants depend on incomes a slim proportion of yield over time. Accepting a right away 230 foundation level loss on the spot leg of the commerce instantly evaporates a big portion of the technique's anticipated annual return.

Until confronted with a catastrophic margin name, arbitrage desks passively liquidate positions naturally over days or even weeks to protect capital.

Second, the structural exigencies of commerce will not be completely according to delta-neutral administration. Intermarket sweep orders and excessive bulk reductions are attribute of distressed or deeply convicted directional sellers relatively than market-neutral yield farmers.

Lastly, the futures market was the last word clincher. IBIT's block of 29.21 million shares is price roughly 18,500 Bitcoins. If arbitrageurs have been to exit delta-neutral positions of this dimension, they would wish to concurrently purchase again roughly 3,700 Chicago Mercantile Alternate (CME) Bitcoin futures contracts to even out the books.

However CME's order e book barely registered a pulse on the day. Solely 91 futures contracts switched trades on the precise second the ETF block crossed the tape. In all the 30-minute window surrounding the deal, simply 1,000 contracts have been executed.

Furthermore, a real foundation unwind of this dimension would have required virtually half of CME's whole day by day buying and selling quantity to be absorbed immediately, which might have triggered a big and extremely seen spike in futures buying and selling.

Subsequently, the truth that no such spike existed in any respect confirms that sellers have been merely lengthy Bitcoin and immediately needed to promote Bitcoin.

Who’s the whale?

Given the size of the transaction, the listing of suspects is surprisingly quick.

NYDIG famous that the block trades exceeded the whole disclosed holdings of all 13F traders within the first quarter of 2026. Nonetheless, this excludes approved members and market makers who maintain stock solely for the aim of offering liquidity relatively than for funding functions.

After a deal of this dimension, analysts naturally look to the move of funds to trace the aftermath. IBIT recorded internet redemptions of $192 million on Could 26, adopted by an extra $528 million in redemptions on Could 27.

Nonetheless, market mechanics recommend that these numbers don’t symbolize direct and instant settlement of whale shares.

The ETF's internet asset worth closed at $42.95 on the day of the commerce and at $42.43 the next day, which was considerably decrease than the negotiated block execution worth of $43.16, and the counterparties who bought the shares had no financial incentive to right away redeem the shares with the issuer.

That manner, your loss might be fastened instantly. As an alternative, the customer might have absorbed the block into stock and systematically distributed the shares to the secondary market over time.

Subsequently, the last word identification of the vendor and his motives stay hidden within the opacity of off-exchange buying and selling. It’s inconceivable to definitively show whether or not the whales have been pushed out by strict inner danger limits or made discretionary bets that the crypto market was headed for a sustained downturn.

Market headwinds and institutional fatigue

After the Could 26 commerce, Bloomberg ETF analyst Eric Balciunas argued that “the market has absorbed the sell-off properly.”

However the timing of the $1 billion exit turned out to be aggressive, as Could was a painful month for digital belongings. The highest cryptocurrency fell practically 4% over the month, ending up buying and selling at practically $73,000, in response to information from CoinGlass.

This worth efficiency was exacerbated by a collapse in investor urge for food for spot Bitcoin ETFs.

NYDIG famous that US funds that participated within the Could 26 commerce have already suffered six consecutive days of outflows. The sector suffered $1.55 billion in outflows throughout this era alone, with BlackRock's IBIT bearing the brunt of the injury, dropping about $1.1 billion.

By the tip of Could, the injury had unfold additional. U.S.-listed spot Bitcoin ETFs recorded whole month-to-month outflows of $2.4 billion, in response to information from SoSoValue.

Resulting from sustained promoting strain, whole belongings below administration throughout the ETF class fell from greater than $100 billion to $94.17 billion.

(Tag Translation) Bitcoin